Adjustable rate home loans (ARMs) consist of any home loan where the rate of interest can alter while you're still repaying the loan. This means that any increase in market rates will raise the debtor's month-to-month payments, making it more difficult to budget plan for the cost of real estate. Still, ARMs are popular due to the fact that banks tend to offer lower rates of interest on an ARM compared to a set rate mortgage.

While the majority of individuals will wind up with a traditional mortgage with a fixed or adjustable rate as described above, there's a wide variety of options indicated for diplomatic immunities. FHA and VA home loan loans, for instance, require much smaller sized down payments from borrowers or no deposit at all from veterans.

For house owners who see their current property as an investment or a source of capital, variations like the interest-only home loan and the cash-out home mortgage offer increased financial flexibility. For instance, paying simply the interest charges on a home loan implies you won't make development repaying the balance. However, if you intend on offering your home in a couple of years, interest-only mortgages can help lessen monthly payments while you wait.

Individuals often rely on cash-out home loans as a Go to this site way to meet big expenditures like college tuition. While the terms of home loans are fairly standardized, lending institutions change the home loan rates they use based upon numerous factors. These consist of info from the customer's financial history, in addition to bigger figures that show the present state of the credit market.

Indicators on How Do Balloon Mortgages Work You Need To Know

The more you pay at the beginning of a home mortgage, the lower your rate will be. This happens in two ways: deposit portion and the purchase of home mortgage "points". Lenders consider mortgages to be riskier if the customer's deposit is smaller sized, with standard loans needing at least 20% down to prevent the added month-to-month expense of personal mortgage insurance.

Purchasing points on your home mortgage implies paying a repaired fee to minimize the interest rate by a set quantity of portion points, normally around 0.25% per point. This can assist homeowners lower their monthly payments and conserve cash in the long run. Each point will generally cost 1% of the overall cost of the home, so that a $400,000 purchase will feature $4,000 home loan points.

Your credit report affects the home mortgage rates loan providers are willing to use you. According to FICO, the distinction can vary from 3.63% to as high as 5.22% on a 30-year set rate mortgage depending on which bracket you fall into. FICO Score15-Year Fixed30-Year Fixed760-8502.87% 3.63% 700-7593.10% 3.85% 680-6993.27% 4.03% 660-6793.49% 4.24% 640-6593.92% 4.67% 620-6394.46% 5.22% Keeping close track of your credit report is an excellent practice whether you're considering a home loan in the near future, and it never injures to start developing credit early.

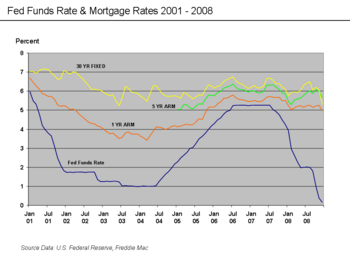

Finally, lending institutions like banks and cooperative credit union all keep a close eye on the present state of the larger market for getting credit. how do reverse mortgages work in florida. This includes the rates at which corporations and governments sell non-mortgage instruments like bonds. Since home mortgage lenders themselves require to spend for the cost of obtaining cash, the mortgage rates they provide go through any modifications because underlying expense.

An Unbiased View of How Arm Mortgages Work

While you can't control the motion of debt markets as a specific, you can watch on where they're headed. The shopping process for home mortgages will be rather different for novice home purchasers and existing homeowners. Purchasers should think about not only the mortgage however the residential or commercial property and their long-term plans, while existing house owners may just want to refinance at a better rate.

We 'd advise comparing loan providers or going through a broker to obtain a pre-approval letter, learning how much banks are ready to lend you, and identifying how inexpensive your typical month-to-month home mortgage would be. This method, when you discover your home, you will have the majority of your ducks in a row to send your quote.

For circumstances, somebody seeking to move after 5 years may seek a 5/1 ARM or an interest-only home loan in order to reduce month-to-month payments till the balance is paid off early by selling the home. Individuals who prepare to live in one home till they totally own it will rather opt for an excellent fixed rate lasting 15 or thirty years (how mortgages work).

Few individuals go through the house buying experience more than one or two times in their lives, and their inexperience means that realtors often play more of an assisting function. As an outcome, lots of home buyers end up picking a home loan loan provider referred by their property representative. While this arrangement appropriates most of the times, remember that a realtor's priorities are to protect quick approval, not to negotiate your benefit rate.

Rumored Buzz why did chuck get cancelled on How Do Negative Interest Rate Mortgages Work

Refinancing your home mortgage when market rates are low can be a great method to reduce your monthly payments or the overall cost of interest. Unfortunately, these two objectives lie in opposite instructions (how do reverse mortgages work). You can lower regular monthly payments by getting a lower-rate home loan of the same or greater length as your present loan, but doing so typically implies accepting a higher expense in overall interest.

Amortization, the procedure of splitting payments in between interest and principal, exposes how early payments mainly go towards interest and not to lowering the principal balance. This suggests that starting over with a brand brand-new home loan however appealing the rate can set you back in your journey to complete https://b3.zcubes.com/v.aspx?mid=5110713&title=h1-styleclearboth-idcontent-section-0indicators-on-which-of-the-following-statements-is-tru ownership. Fortunately, lending institutions are required to offer you with comprehensive quotes outlining estimated rate, payment schedules and closing costs.

A mortgage is a contract that permits a customer to utilize residential or commercial property as collateral to protect a loan. The term describes a home loan for the most part. You sign an agreement with your lender when you obtain to buy your house, providing the loan provider the right to do something about it if you don't make your needed payments.

The sales earnings will then be utilized to pay off any financial obligation you still owe on the residential or commercial property. The terms "mortgage" and "home mortgage" are typically used interchangeably. Technically, a home loan is the arrangement that makes your mortgage possible. Realty is expensive. The majority of people don't have adequate readily available cash on hand to buy a home, so they make a down payment, ideally in the area of 20% or two, and they borrow the balance.

Everything about How Mortgages Subsidy Work

Lenders are only happy to give you that much cash if they have a way to decrease their danger. They safeguard themselves by requiring you to use the home you're buying as security. You "promise" the residential or commercial property, and that promise is your home mortgage. The bank takes permission to put a lien against your house in the small print of your agreement, and this lien is what allows them to foreclose if necessary.

A number of kinds of home loans are available, and understanding the terminology can assist you choose the ideal loan for your circumstance. Fixed-rate home loans are the easiest type of loan. You'll make the very same payment each month for the whole term of the loan. Fixed rate home mortgages usually last for either 15 or 30 or 15, although other terms are available.